America’s Immigration Dilemma

Vantage Point: Mini Briefs from The Terry Group and the Global Aging Institute

April 18, 2024

It’s not surging productivity or surging labor-force participation that’s driving today’s surprisingly resilient economic expansion. It’s surging immigration, which is becoming ever more critical to growth as America ages.

When the Federal Reserve first began to raise interest rates in March 2022, most economists predicted that the United States would soon fall into recession. Two years later and counting, it still hasn’t. While this is good news, what’s driving today’s surprisingly resilient economic expansion poses something of a dilemma for policymakers.

It’s not surging productivity growth that’s driving it. Nor is it surging labor-force participation rates. It’s surging immigration. In other words, the same development that has unleashed chaos at the southern border, overwhelmed the asylum system, and overburdened state and municipal governments is also what has helped the U.S. economy defy gravity in the face of rising interest rates and ebbing fiscal stimulus.

The economics of immigration are clear enough: America, with its rapidly aging population, benefits from more of it. But so are the politics of immigration: As the border crisis drags on and on, surveys show that America increasingly wants less of it. The circle could be squared by clamping down on unauthorized immigration while expanding opportunities for legal immigration. Alas, the polarization of our political system may preclude such a sensible solution.

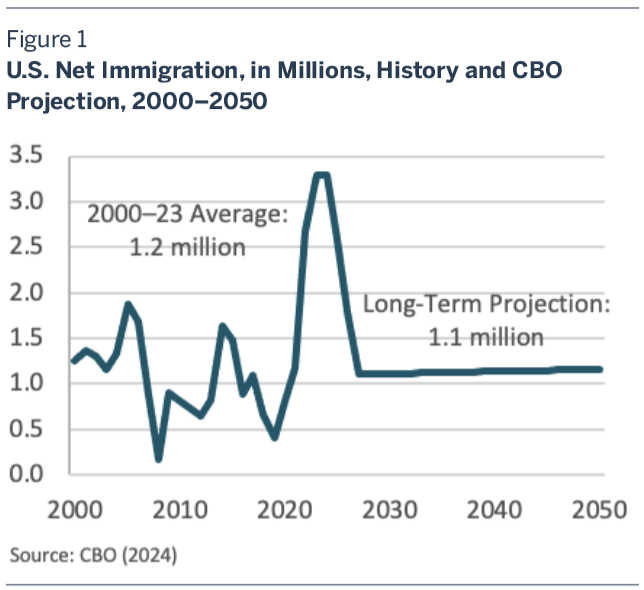

A Rollercoaster Path

It is hardly news that America is experiencing an unusually large wave of immigration. Net immigration (in-migration minus out-migration) has followed a rollercoaster path in recent decades, rising and falling as the economy expands and contracts and policy becomes more or less restrictive. Since the end of the pandemic, it has surged. According to the CBO, net immigration reached 3.3 million in 2023, an all-time historical high and nearly three times its annual average of 1.2 million since 2000.1 (See figure 1.)

What is much less appreciated is that the current immigration wave has played a central role in driving the growth in U.S. employment and GDP. Although most migrants arriving at the southern border gain entry to the United States by claiming asylum, most are in fact labor-market migrants looking for jobs. The majority receive authorization to work within six months, and many of those who don’t work illegally.

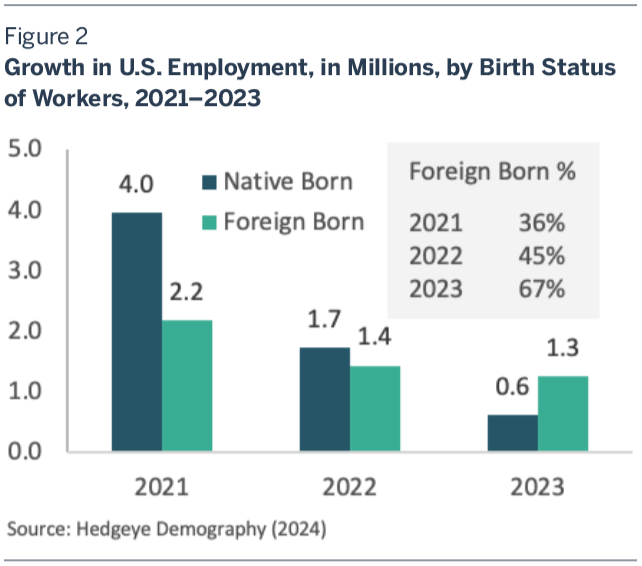

During the initial stages of the post-pandemic recovery, the growth in U.S. employment was mostly driven by falling unemployment and rising labor-force participation among native-born workers. By 2022, however, both the unemployment rate and the labor-force participation rate were just about back to where they were before the pandemic. Still, employment has continued to grow, mainly because the number of foreign-born workers has continued to grow. According to an analysis of Current Population Survey data by Hedgeye Demography, foreign-born workers accounted for 36 percent of the total growth in U.S. employment in 2021. In 2022 they accounted for 45 percent of it and in 2023 they accounted for 67 percent of it.2 (See figure 2.)

Like other immigration waves before it, the current wave will eventually crest and recede. On the “push” side of the immigration equation, economic and political conditions in the countries migrants are coming from may improve. On the “pull” side, some combination of economic developments may finally plunge the United States into recession. Immigration policy may also become more restrictive, as seems increasingly likely to happen whichever party controls the White House next year.

In its latest budget projections, the CBO assumes that net immigration will remain at its current elevated level for another year, then decline rapidly to 1.1 million, close to its long-term average.3 The economic impact of the current immigration wave, however, will likely prove more lasting than the wave itself. According to the CBO, the U.S. labor force a decade from now will still be more than 5 million larger than it would be had immigration not surged.

No Substitute

All of this underscores the critical importance of immigration to economic growth in an aging America. Back when the United States had a replacement-level fertility rate, immigration was what kept the labor force growing. For the foreseeable future, it will be all that keeps the labor force from contracting.

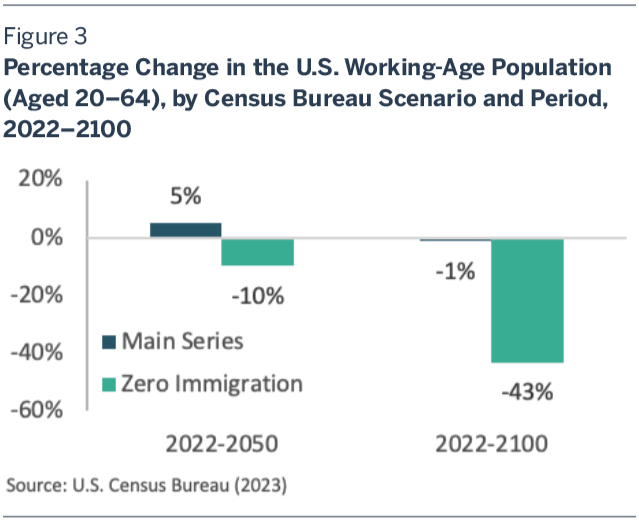

The Census Bureau’s latest population projections leave no doubt that this is the demographic reality America now faces.4 In its “main series,” which serves as its official projection, the Census Bureau assumes that in the future net immigration will average 0.9 million a year, only a bit less than the long-term level that the CBO assumes in its projections. Even so, the U.S. working-age population registers no growth over the rest of the century. Without any net immigration at all, the assumption in the Census Bureau’s zero immigration scenario, the U.S. working-age population would enter a steep decline. By 2050, it would be 10 percent smaller than it was in 2022. By 2100, it would be 43 percent smaller. (See figure 3.)

While many Americans may wish that it weren’t so, there is little if anything that could substitute for immigration as a long-term driver of economic growth. Labor-force participation by adults in the traditional working years is at a ten-year high, and labor-force participation by the elderly, which was a big driver of employment growth in the 2010s, is no longer rising. One reason may be that the pandemic caused older workers to reconsider late in life trade-offs between work and leisure. More importantly, Boomers are beginning to age out of their sixties and early seventies into their late seventies and eighties, when both ability and desire to work fall off steeply.

Nor, all the hype about AI notwithstanding, is a productivity revolution likely. As we explained in a recent issue brief (“Why the Collapse in U.S. Population Growth Matters”), there are plenty of reasons to think that productivity growth is more likely to slow down than to speed up in an aging America in which fiscal burdens will be rising, investment rates will be falling, and a more slowly growing and graying workforce is likely to be less flexible, less mobile, and less entrepreneurial.

Higher birthrates would of course help considerably in the long run. But the U.S. total fertility rate has fallen almost every year since the Great Recession. As of 2022, it stood at just 1.66, down from 2.12 in 2007. As we explained in another recent issue brief (“America’s Rapidly Deteriorating Demographic Outlook”), there is little reason to think that a rebound is likely any time soon. And even if birthrates were to surge starting tomorrow, it wouldn’t have a significant impact on employment or economic growth for at least twenty-five years.

Balancing the Books

Faced with a similar calculus, many developed countries are increasingly relying on immigration to balance their demographic and economic books, and a few, notably Australia and Canada, have made it the lynchpin of their long-term strategies for addressing the aging challenge.

The purpose of this issue brief is neither to propose nor to endorse a particular immigration reform plan. It seems clear to us, however, that any successful plan will need to recognize both the economics and the politics of immigration. The obvious, and perhaps only, way forward is to proceed on two fronts at once—tightening border security to stem the flood of unauthorized immigration while creating new opportunities for legal immigration.

It may be delusional to hope that our political economy is still capable of the kinds of trade-offs such a plan would involve. But if we fail to rise to the occasion, tomorrow’s aging America will be a less dynamic, less hopeful, and less prosperous country than it could and should be.

About Vantage Point

Vantage Point is a sister publication of Critical Issues. Both publications explore the demographic and economic trends reshaping America and the world, and in particular the future environment for retirement and health care. While Critical Issues offers in-depth analyses of these trends, Vantage Point features mini briefs on important new developments.

Project Supervisor

Tom Terry, CEO, The Terry Group

Series Author

Richard Jackson, President, the Global Aging Institute (GAI)